By the ETF research team at Invesco.

Investing in UK equities shouldn’t be so taxing

With the Brexit leaving date quickly approaching, how is your portfolio positioned?

If you are considering gaining exposure to UK equities, do you want to focus on the largest companies (FTSE 100) that generate earnings from all around the world or medium-sized companies (FTSE 250) that generate more of their earnings from domestic markets?

Whatever your view, a passive ETF can offer efficient, low-cost exposure to the index.

Structure matters

A passive ETF can replicate an index physically or synthetically. The physical method involves buying and holding all (or a sample) of the constituents of the index and rebalancing whenever the index does. The attraction for many investors is the simplicity, in terms of understanding how it works, and being able to explain it to clients.

The synthetic method also involves holding a basket of securities but not necessarily those of the reference index. The ETF will aim to achieve the index performance by using derivatives with the swap counterparties agreeing to pay any difference between the returns of the securities basket and the index. The objective of the synthetic model is to deliver a closer return to the index, i.e. low tracking error and typically with low costs.

Costs matter

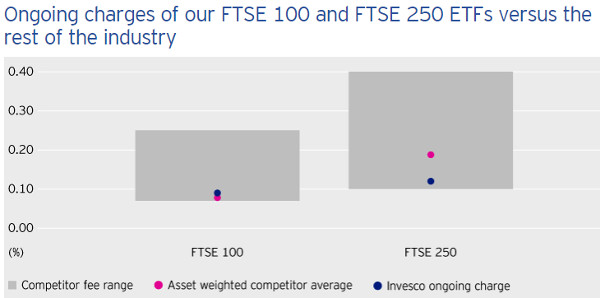

Cost is one of the most obvious contributors to performance and, all else being equal, the lower the cost, the better the potential performance should be. We have recently reduced the annual charge on our FTSE 100 and FTSE 250 UCITS ETFs to 0.09% and 0.12% p.a. respectively. Here’s how the funds compare to competitors.

Source: Invesco.

While an ETF’s ongoing charge is plain to see, some other costs may be less obvious, such as those related to rebalancing. You can compare ETFs tracking the same index by looking at how closely each ETF matches the index performance over time (“tracking difference”) and how volatile the relative performance is from day to day (“tracking error”). These calculations are usually based on the ETF’s end-of-day NAV. However, this does not always tell the whole story: in the case of UK equity ETFs, the truth can make a big difference.

UK equity ETFs

When considering the total cost of replicating a UK equity index, the synthetic structure may gain the upper hand by not having to pay Stamp Duty.

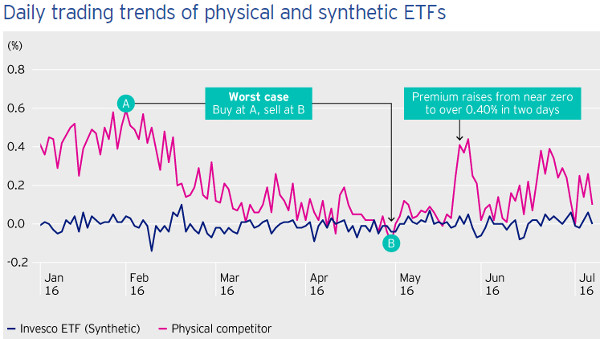

An investor buying an ETF on the secondary market does not have to pay Stamp Duty directly but a physically-replicating ETF will generally be subject to the 0.50% tax when purchasing the underlying securities. This is reflected in the creation cost of the fund and may help explain the difference between the ETF’s market price and its NAV. When an ETF sees net inflows from investors, the market price generally trades at a premium to NAV. As illustrated in the chart below, the premium for a physically replicated FTSE 100 ETF could be as high as 0.60% over NAV.

For a synthetically replicating ETF, the swap counterparties (generally large banks) purchase the replicating portfolio, not the fund. As this transaction is executed as part of the hedging of the swap contract, the banks are generally exempt from Stamp Duty.

As the following chart shows, synthetically-replicated ETFs (the Invesco FTSE 100 UCITS ETF is used for illustrative purposes) often trade close to NAV, whereas physically-replicated funds may see sharp swings depending on flows. The net impact could be an up-front saving to the end-investor in synthetic ETFs.

Source: Invesco.

The worst-case scenario is when you invest in a physically-replicated UK equity ETF when other investors are also buying, meaning units are having to be created, incurring Stamp Duty, and then selling when others are either selling or at least not investing as much, meaning there is no longer a premium. On a round trip, this could potentially cost you the equivalent of 0.50% to 0.60% in performance, having a much larger impact on performance than fees or spreads.

| FEATURED ETFs

Invesco FTSE 100 UCITS ETF Invesco FTSE 250 UCITS ETF |

Conclusion

There is not one replication method that is best in all markets and, as such, we look at each product on a case-by-case basis. For the UK equity market, the specific characteristics related to Stamp Duty can give the synthetic replication method a structural advantage over physical, making investing in UK equities a less-taxing experience. Please get in touch if you would like to find out more.

Managing risks

Both replication models can be exposed to counterparty risk and would normally have certain measures in place to limit the impact of a default. Invesco’s synthetically-replicated ETFs manage counterparty risk by:

- Using up to four counterparties for the swap contracts

- Allowing only high-quality securities in the basket

- Resetting the swaps to zero when certain events are triggered

(The views expressed here are those of the author and do not necessarily reflect those of ETF Strategy.)