By Nick Leung, Research Analyst at WisdomTree.

Nick Leung, Research Analyst at WisdomTree.

Optimised Commodities: Delivering Alpha with Lower Volatility

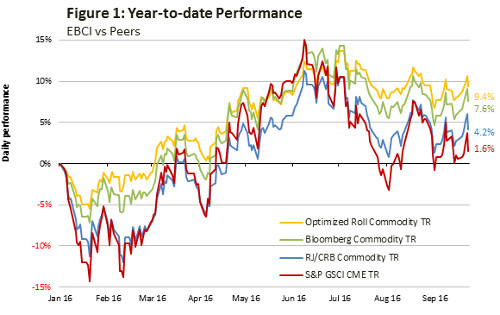

Broad commodity prices have recently shown signs of recovery after falling by over 50% between 2011 and 2015. The BNP Paribas Optimised Commodity Index (EBCI) has returned over 9% year-to-date, outperforming other broad commodity strategies including the Bloomberg Commodity Index (BCOM) and Thomson Reuters CRB by close to 200 bps. This outperformance reflects the two fundamental components on which the strategy is built upon, and this brief will explore how diversified commodities exposure coupled with futures curve optimisation have suppressed volatility whilst delivering alpha versus other commodity strategies on a year-to-date basis.

Controlling Volatility Through Sector Capping

One of the major benefits of broad commodity baskets is the comparatively lower volatility against single commodities. At the heart of this lies the uncorrelated nature of individual commodities to one another which, once combined into a single basket, allow for large price movements to be offset against one another. A more diversified basket results in drastically reduced volatility, and this explains why at 13%, the annualised volatility of well-diversified commodity baskets can be lower than even gold (17%).

The EBCI Index draws upon this principle by employing a broad-based and sector-balanced approach to commodities investing. Through adopting BCOM starting weights at each annual rebalance in January, and by implementing stringent sector caps of 35%, the basket accommodates for a more even representation of individual commodities.

Source: WisdomTree. Data as of 31 August 2016.

Without such caps, strategies such as the Thomson Reuters CRB and S&P GSCI end up with significant overexposure to particular sectors like energy, which can typically comprise up to 60% of the basket, and induces higher volatility for investors.

Indeed, the 2016 trend in crude oil prices showcases how this can be the case, with oil continuing to succumb to heightened volatility on the back of constant supply and demand speculation. As shown in Figure 1, commodity baskets with large energy exposures (CRB and S&P GSCI) have been penalised for this overexposure, benefitting from prices rallies but also participating in price crashes. As a result, such strategies have not only underperformed but also offered greater cyclicality.

Since the basic rationale for strategic allocations into broad commodities is typically based upon asset allocation needs, i.e. reducing volatility of conventional equity and bond portfolios, poorly diversified commodity strategies can actually undermine the fundamental reason for investing in broad commodity strategies. Because of this, investors should seek to avoid overexposure to particular sectors by considering commodity strategies with a balanced sector weighting mechanism.

Generating Alpha through Futures Curve Optimisation

Whilst individual commodity weights are hugely influential in determining the risk-return profile of overall strategies, perhaps of equal importance when considering long-term commodity investments is the roll return or cost of carry component. This represents a source of additional return (or drag on returns) that commodity investors are inevitably exposed to and yet is something which is often either overlooked or not fully understood.

Conventional broad commodity strategies, including the BCOM and CRB, typically employ a simple approach to rolling out futures contracts: replacing expiring contracts with near-month contracts that are slightly further out along the futures curve. In doing so, such strategies tend to be highly exposed to the front end of the futures curve for any given commodity, and this has significant implications for investors.

In times of backwardation, exposure at the front end of futures curve is ideal as this tends to be precisely where the slope is steepest, and where the positive roll return can be maximised. Conversely, investors can incur significant costs when commodities are held strategically over long investment periods whilst in contango, with the front of the curve being where the cost of carry is greatest.

The optimised roll strategy departs from conventional rolling methodologies by holding futures exposures depending on the shape of the underlying commodities’ futures curve. Broadly speaking, when individual commodity markets are in contango, an optimised roll strategy would be invested in futures contracts further out where the slope of the futures curve is shallower (and where time and rolling erodes futures prices less). As such, investors suffer less from cost of carry than in the case of a conventional rolling. In times of backwardation, the flexibility of the optimisation methodology would allocate at the front of the curve.

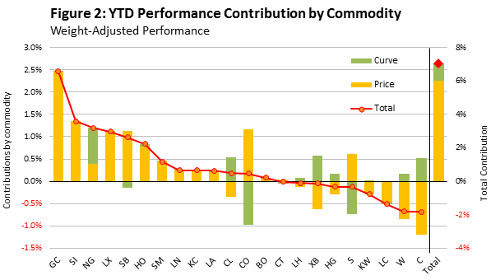

Taking a look at the year-to-date performance attribution by commodity, we can get a sense of just how significant curve optimisation can be in generating alpha for investors.

Source: WisdomTree. Data as of 31 August 2016.

Take natural gas for example. Figure 2 shows that whilst the 26% YTD rise in price contributed 0.4% to the overall performance of the EBCI strategy, the curve enhancement actually contributed over twice as much at 0.8%. In fact, across the spectrum of commodities, curve enhancements have been similarly effective in soybean and WTI, working to either dampen falls in price or provide an additional layer of return. On an aggregated basis, curve enhancement contributions across all commodities delivered over 100 bps in additional performance, presenting a case as to how curve enhancement strategies can indeed generate alpha versus conventional strategies.

Alongside minimising the cost of carry, allocating further out in the curve also provides investors an added benefit of hedging against, or at least dampening, large price swings that arise from speculative activity. This is because positions further out in the curve tend to be less sensitive to immediate spikes in volatility, being more reflective of longer-term supply and demand dynamics. This, coupled together with a well-diversified basket, can suppress volatility well below that of comparable strategies.

In an investment horizon where asset class prices are becoming increasingly volatile and correlated, broad commodity baskets offer investors a means to decorrelate investment portfolios and reduce overall volatility. Alongside this, the consideration of an optimised roll strategy may also potentially complement multi-asset portfolios by giving the investors better diversification and improved returns.

Investors sharing this sentiment may wish to consider the WisdomTree Enhanced Commodities UCITS ETF (WCOA). This LSE, Xetra and Borsa Italiana-listed fund seeks to track the performance, before fees and expenses, of the BNP Paribas Optimised Roll Commodity Total Return Index. The fund also aims to outperform the Bloomberg Commodity Index TR over the long term. It invests in US Treasury Bills and uses total return swaps to deliver the Index performance. The swaps are collateralised on a daily basis and reset monthly.

(The views expressed here are those of the author and do not necessarily reflect those of ETF Strategy.)